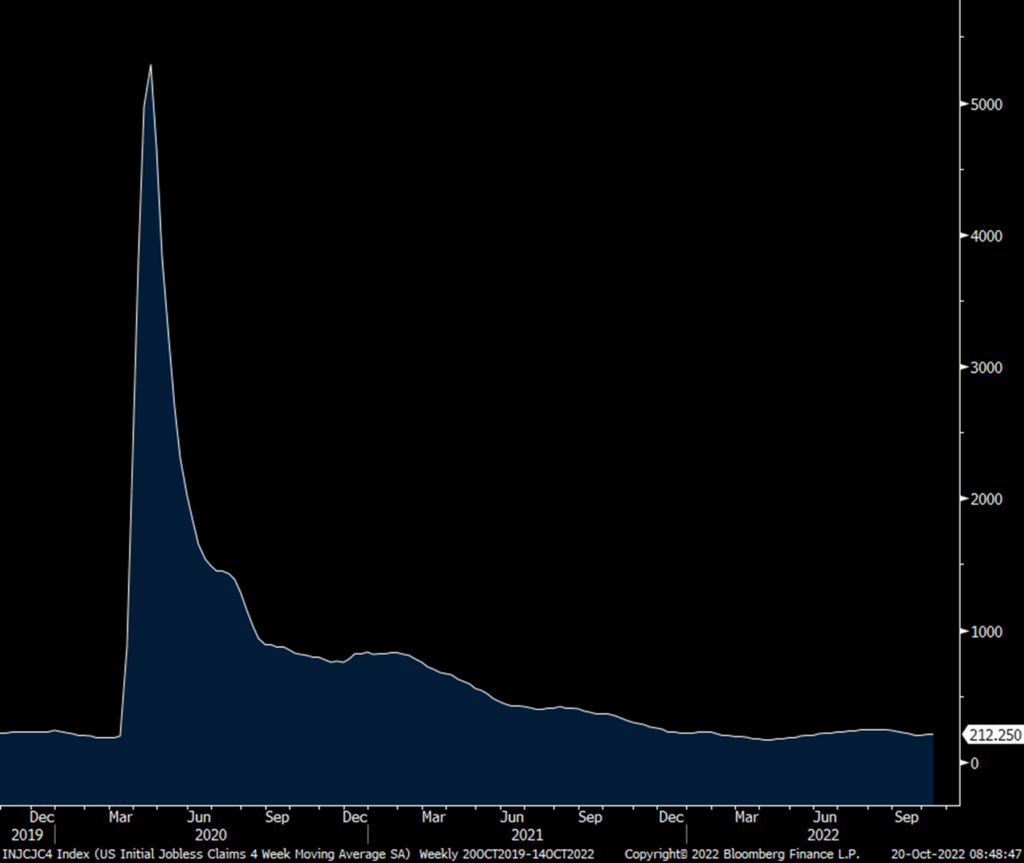

Initial jobless claims fell to 214k, 19k below expectations and down from 226k last week. Continuing clams rose to 1.385mm from 1.364mm and that was just a hair above the estimate. The 4 week average was little changed at 212k vs 211k in the week prior. The bottom line remains the same here, employers are holding on tight to the employees that they have and the tech area that is laying people off are seemingly finding no problem finding a new job or at least are getting a generous severance that will tide them over.

4 Week Avg in Claims

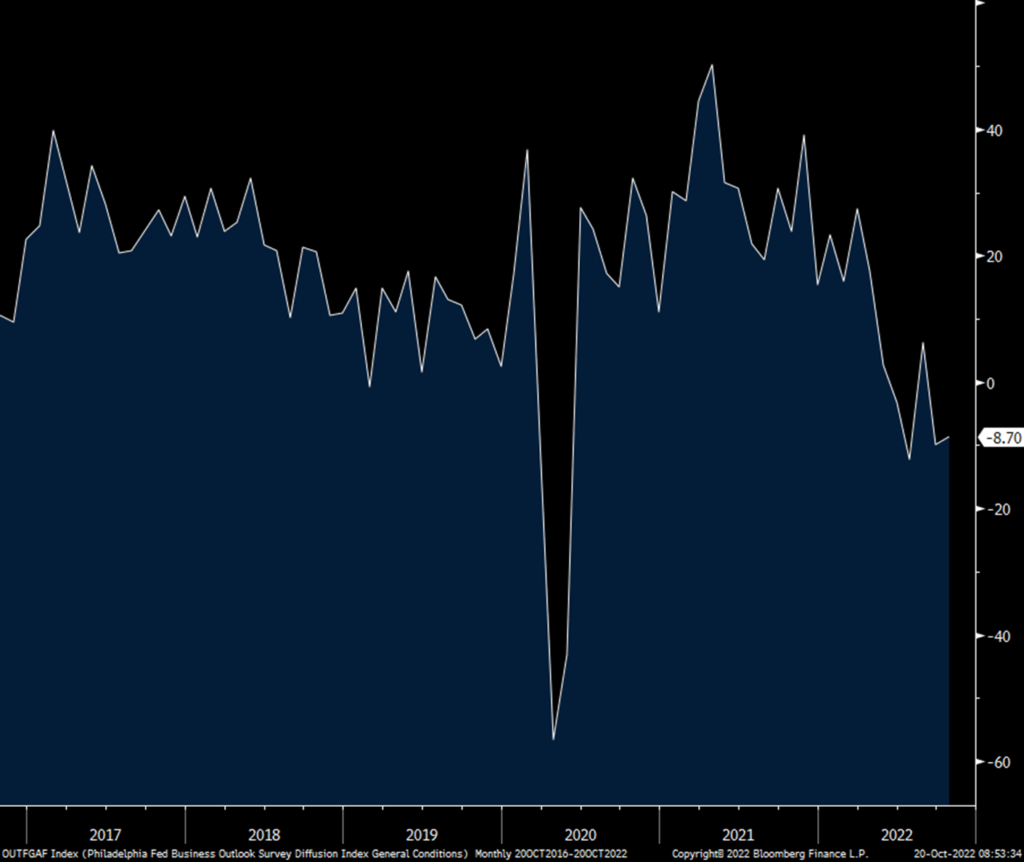

After the negative print seen with the NY manufacturing index for October, today’s Philly index was -8.7 from -9.9 and vs the estimate of -5.0. New orders remained deeply negative at -15.9 vs -17.6 and vs the 6 month average of -9.0. Backlogs too were also below zero at -22.5 vs -28.5 and vs the 6 month average of -9.0. Inventories stayed below zero but a bit less so. Delivery times remained negative while prices paid and received bounced somewhat. Employment improved as did the workweek.

The 6 month business outlook was negative for a 5th straight month and expectations for prices paid and received fell notably. Capital spending plans were little changed.

Bottom line, US manufacturing is in a recession and should be confirmed by the other regional surveys and the national one too.

Philly Fed

Peter is the Chief Investment Officer at Bleakley Advisory Group and is a CNBC contributor. Each day The Boock Report provides summaries and commentary on the macro data and news that matter, with analysis of what it all means and how it fits together.

Peter is the Chief Investment Officer at Bleakley Advisory Group and is a CNBC contributor. Each day The Boock Report provides summaries and commentary on the macro data and news that matter, with analysis of what it all means and how it fits together.