In the BoA conference call yesterday, Brian Moynihan said this on deposits, “As monetary policy tightens on deposits, we see clients with excess liquidity looking for yield, with that being the global banking movements you can see moving from noninterest bearing to interest bearing accounts, or in our wealth manager business, where we saw clients shift out of brokerage suites into preferred deposits or other investment products, like treasuries, that we offer.” The CFO said on a y/o/y basis “The noninterest bearing deposits are down 3%, while the interest bearing are up 4%. So, overall, we grew our deposits” but he did say they fell less than 1% q/o/q. One thing I forgot to mention also yesterday but have stated before, if/when banks lose deposits, the US Treasury market is also losing them as buyers. On the direction of rates on savings/checking accounts, “Do we expect deposit rates to increase? Yes, of course. And we will remain both disciplined and competitive, and that is built into our asset sensitivity.”

As we dig deeper into the earnings picture in the coming month plus, I am pretty confident that the earnings beat will still be around 70% and many will say how great everything turned out but this is the game every quarter where expectations fall enough going in that the bar is easy to beat. The big picture still remains the same in that earnings growth ex energy is slowing.

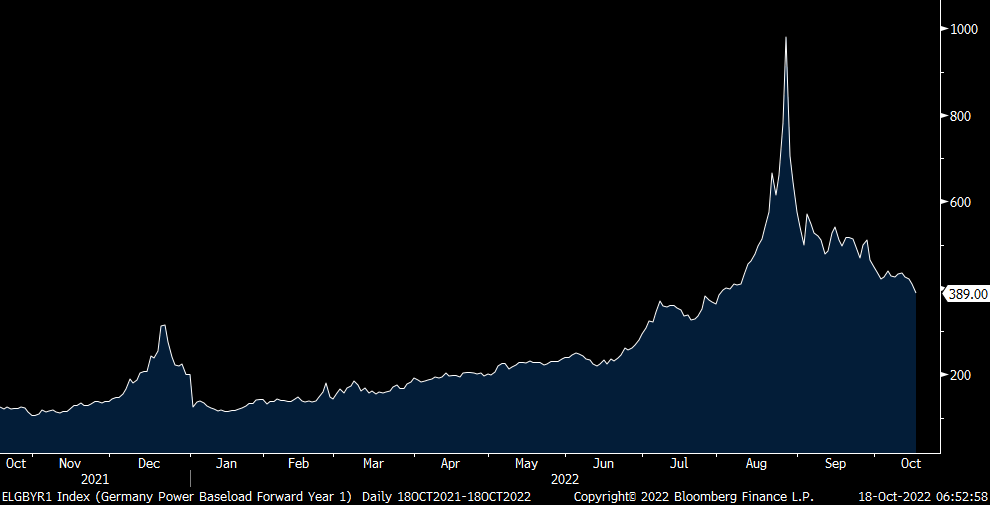

On the heels of the story yesterday that Germany is extending the life of its 3 remaining nuclear plants (powering about 12% of its energy needs) past the end of the year and into Q1 2023, German power prices one yr forward are down 5% today after dropping by almost 3% yesterday. At 389 euros per megawatt, that is the lowest since early August. When physics, chemistry, warmth, money and business don’t matter, you get this comment from the head of the Green Party parliamentary group, “There is no objective reason for this” with regards to keeping these nuclear plants open thru the winter. This, even though nuclear is the cleanest and most reliable base load power and we remain bullish and long uranium.

The Dutch TTF natural gas price is lower too, down by almost 5% to the lowest since June, after yesterday’s 12% drop and by 23% over the past week and just maybe the Europeans can make it thru the winter ok, albeit still expensively. The sentiment is so dour on Europe and the euro that if they can, there is an opportunity here in stocks and the currency there. On the other hand, European bonds still remain highly unattractive and are weaker today with yields higher.

German Power one yr forward

Dutch TTF

The October German ZEW investor expectations index rose to a still deeply negative -59.2 from -61.9 and that was better than the feared further decline to -66.5. The Current Situation though deteriorated again to -72.2 from -60.5, the lowest since August 2020. ZEW said simply, “Despite the slight rise in expectations, the economic outlook for Germany has thus deteriorated significantly.”

German ZEW

The FT has a story today titled “BoE set to further delay sales of government bonds until markets calm” and soon after a spokesperson for the BoE said “This morning’s FT report that the BoE has decided to delay MPC gilt sales (QT) is inaccurate.” The plan of the BoE is to shrink their balance sheet by 80b pounds over the next 12 months from those maturing combined with sales. Their balance sheet totals about 950b pounds. The 10 yr gilt yield is up 5 bps after falling by 36 bps yesterday. The pound is lower by .7% after yesterday’s 1.7% rally. Again, UK stocks and the pound are dirt cheap.

Peter is the Chief Investment Officer at Bleakley Advisory Group and is a CNBC contributor. Each day The Boock Report provides summaries and commentary on the macro data and news that matter, with analysis of what it all means and how it fits together.

Peter is the Chief Investment Officer at Bleakley Advisory Group and is a CNBC contributor. Each day The Boock Report provides summaries and commentary on the macro data and news that matter, with analysis of what it all means and how it fits together.