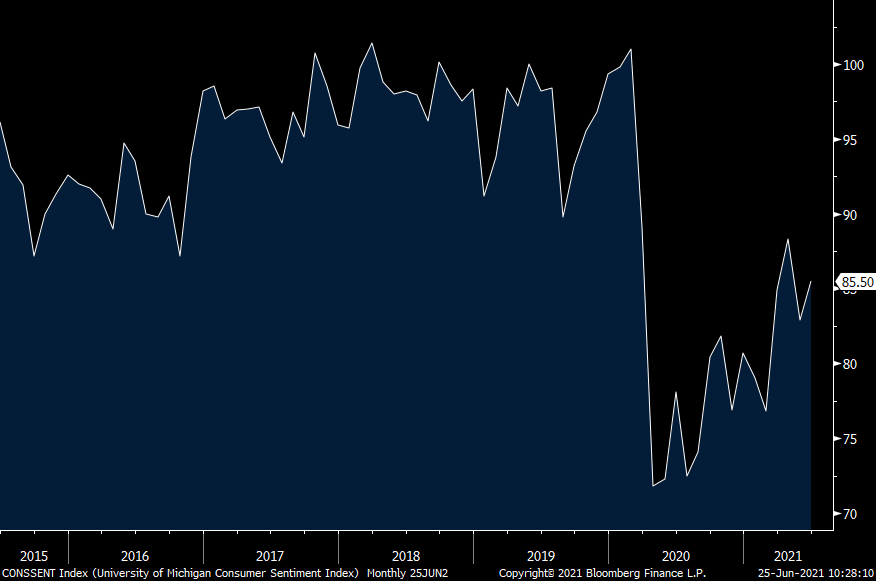

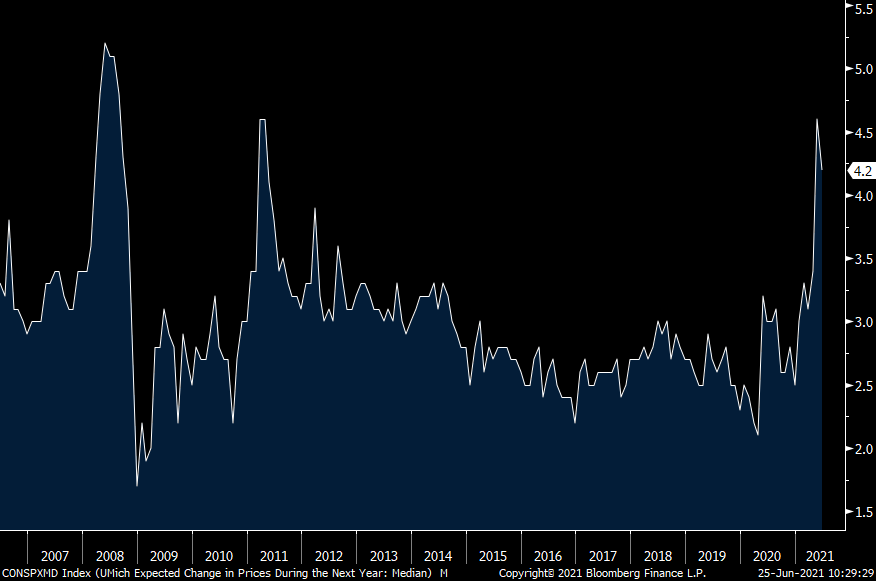

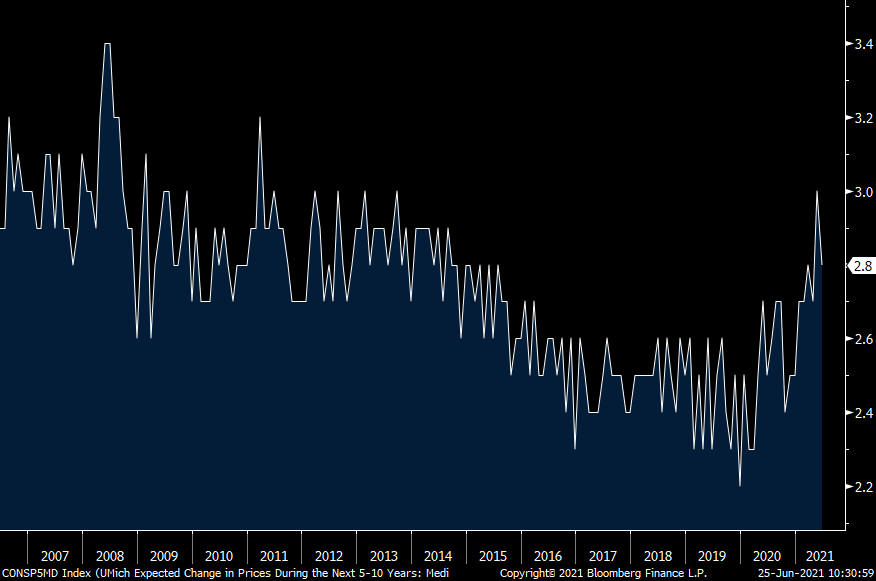

The final June UoM consumer confidence index was 85.5 vs the 1st print of 86.4 and that compares with 82.9 in May, 88.3 in April and 84.9 in March. The internals were mixed as Current Conditions fell .8 pts m/o/m but was offset by a rise to 83.5 from 78.8 in Expectations. One year inflation expectations came in at 4.2% vs the initial June read of 4% and vs 4.6% in May, 3.4% in April and 3.1% in March. That’s the 2nd highest level in 10 years. Gas prices are a key factor in this and while gas prices are at the highest level since 2014 according to AAA, less people think that will continue. I unfortunately believe they will be wrong as I expect even higher energy prices in the quarters to come. Not only is the Wall Street consensus and within the Fed that the current pace of inflation gains is transitory, consumers feel the same as longer term expectations came in at 2.8% vs 3% in May and the UoM said “consumers also believed that the price surges will mostly be temporary.” As the WSJ said, “let’s pray.”

Employment expectations continued to improve as they should. Income expectations though have been little changed as this component came in at 16 vs the 1st print of 15 and vs 18 in the two prior months. In fairness though, it was 8 in March and 6 in February. Also, “The highest income expectations were anticipated by younger households, who expected income gains of 4.1%.”

Spending intentions fell sharply m/o/m because of sticker shock. Those that said it’s a good time to buy a home fell 16 pts m/o/m to 74. It was 125 in March. Those that want to buy a vehicle fell 13 pts m/o/m to 87. It was 114 in March and 118 in April. There was no change in those that said it’s time to buy a major household item at 112 but it was 126 in April and 128 in March. For cars and homes, those are the lowest levels since 1982.

As said here all year, one’s political bias highly influenced their level of confidence. Confidence for Democrats in June came in at 104.2, just off its post election high seen in April and is vs 72.4 in October. Republican confidence fell to a new low at 60.3 vs 98 last October.

Finally, depending where you were on the income scale influenced your answers to this survey. UoM said “All of the June gain was among households with incomes above $100,000.” A lot of this is because of muted income expectations for the bottom 3rd of income households at the same time “16% of households in the bottom third of the income distribution complained more often that inflation had already reduced their living standards, three times the 5% recorded among those with incomes in the top third.” Again, inflation hurts the people who can least afford it.

My bottom line is that while confidence has improved with the vaccines and broad reopening, it still remains well below the February 2020 print of 101 vs 85.5 in June. There is obviously still a certain level of uneasiness though something that hopefully will improve in the quarters to come. That said, for at least the bottom third of income earners, higher inflation is a major headwind for their standard of living.

UoM CONSUMER CONFIDENCE

ONE YR INFLATION EXPECTATIONS

5-10 YR INFLATION EXPECTATIONS

Peter is the Chief Investment Officer at Bleakley Advisory Group and is a CNBC contributor. Each day The Boock Report provides summaries and commentary on the macro data and news that matter, with analysis of what it all means and how it fits together.

Peter is the Chief Investment Officer at Bleakley Advisory Group and is a CNBC contributor. Each day The Boock Report provides summaries and commentary on the macro data and news that matter, with analysis of what it all means and how it fits together.