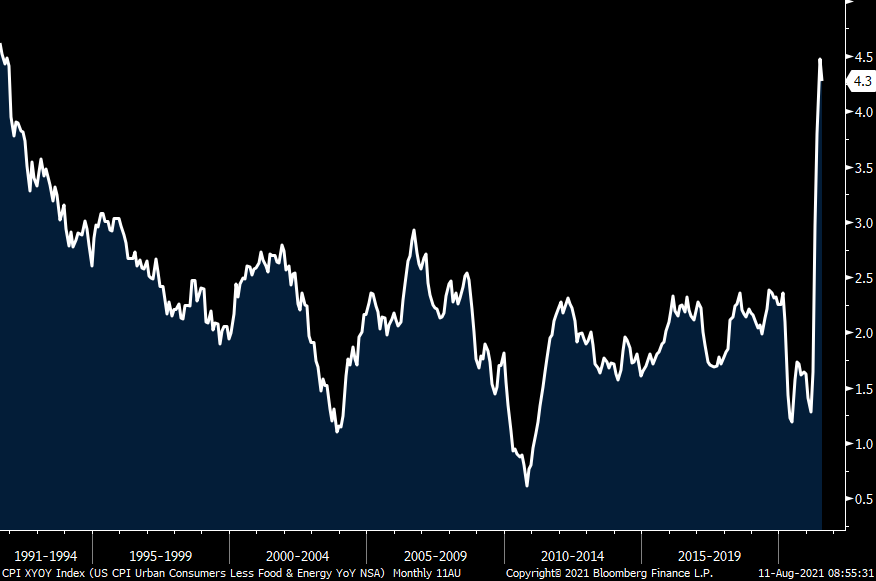

Headline CPI rose .5% m/o/m in July after a .9% increase in June. That was as expected after months of big upside surprises. The core rate was higher by .3% after a .9% spike last month but that was one tenth less than forecasted. Versus last year, headline inflation rose 5.4% and the core rate by 4.3%. The core rate is now running at a 6.4% annualized pace over the past 6 months and is up by 5.9% from July 2019, an annual pace of just under 3%. Food prices rose .7% m/o/m and 3.4% y/o/y while energy prices were higher by 1.6% m/o/m and 24% y/o/y.

While the methodologies are somewhat different, Apartment List said rents in July rose 2.5% from June. The BLS said Rent of Primary Residence was up just .2% m/o/m and Owners’ Equivalent Rent by .3%. So assume now that the big rent increases within the BLS data will only be playing catch up in the quarters to come because nowhere in real life were rents up just .2% in July from June and up by 1.9% y/o/y. Apartment List has rents up 11% just from January thru July while the BLS has OER higher by 2.4% y/o/y.

I point this sector out specifically because it is the biggest component of CPI at about 30% and around 40% of the core. Elsewhere within services medical care costs rose .3% m/o/m after one tenth declines in the two previous months and they are up just .3% y/o/y. It’s been medical care commodities that have kept a lid on things while the cost of physician and hospital services rose between 2.8-3.9% y/o/y. Airline fares saw no change m/o/m but are up 19% y/o/y on easy comps. Overall, services inflation ex energy rose .3% m/o/m and 2.9% y/o/y which really was the trend pre Covid but as stated, rent prices in this survey are about to quickly accelerate.

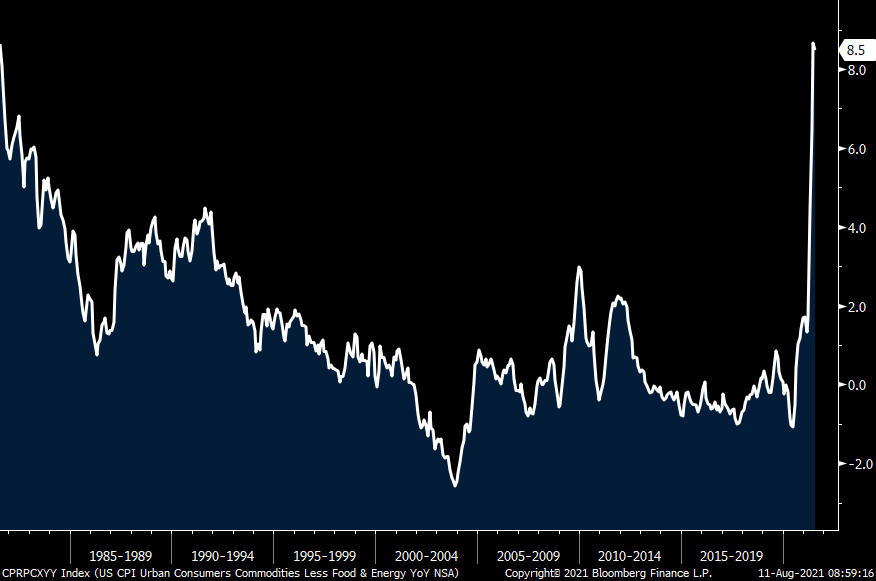

Core goods inflation rose .5% m/o/m and 8.5% y/o/y. That .5% gain comes after rather aggressive price increases in the prior months, specifically 2.2% in June and 1.8% in May. The price of used cars were up just .2% m/o/m but after a 10.5% spike in June and 7.3% gain in May. They are ‘only’ up 42% y/o/y. new car prices jumped 1.7% in the month after a 2% increase in June and are now higher by 6.4% y/o/y. Apparel prices were flat m/o/m but after a .7% gain in June and 1.2% rise in May. They are higher by 4.2% y/o/y.

Bottom line, while we might get some further slowing in used car prices as that seems to be a poster child for the current bout of inflation and a noted talking point of those in the transitory camp, the cost of housing within the government numbers have a lot of catching up to do with reality and thus this inflation story is going to continue so don’t rest easy. The problem also here is that inflation is running faster than wages so we have a drop in REAL wages which is economically contractionary and AGAIN why stable prices is the precursor to strong growth and employment and thus the Fed’s sole focus on the labor market is wrongheaded.

The inflation breakevens out 3, 5 and 10 years are down about 1 bp. The 10 yr after touching 1.37% has backed off to 1.34-.35%. The 5 yr is down by 2 bps to .81% while 2 yr yields are unchanged.

CORE CPI

CORE GOODS PRICES

Peter is the Chief Investment Officer at Bleakley Advisory Group and is a CNBC contributor. Each day The Boock Report provides summaries and commentary on the macro data and news that matter, with analysis of what it all means and how it fits together.

Peter is the Chief Investment Officer at Bleakley Advisory Group and is a CNBC contributor. Each day The Boock Report provides summaries and commentary on the macro data and news that matter, with analysis of what it all means and how it fits together.