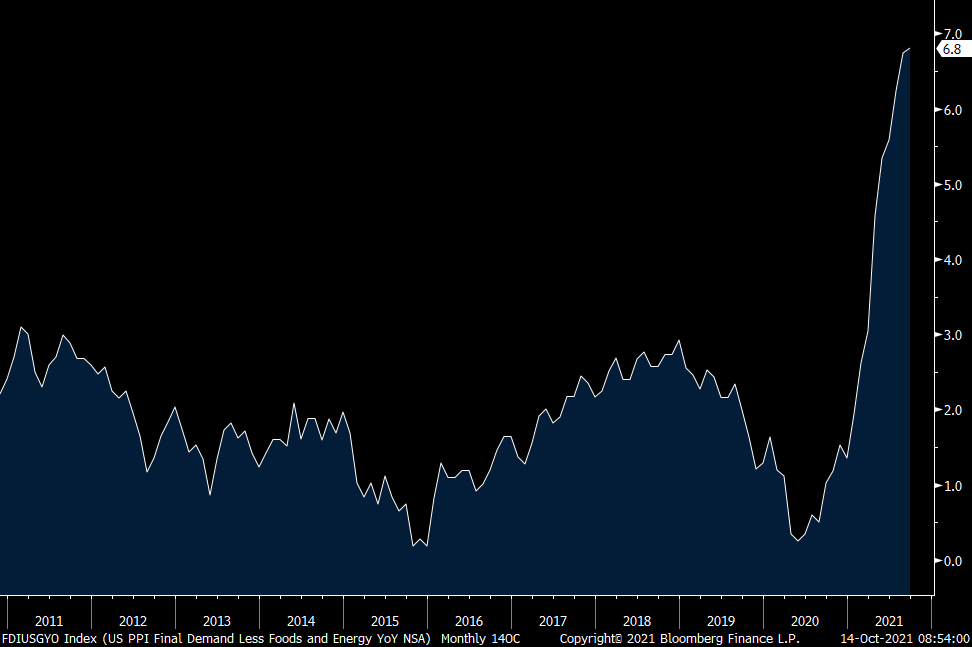

Headline PPI rose .5% m/o/m in September after a .7% increase in August. That was one tenth below the estimate. Taking out food and energy saw a .2% m/o/m gain which was 3 tenths less than forecasted and follows a .6% rise last month. Versus last year, price gains are robust with a headline gain of 8.6% and core increase of 6.8%. Over the past 6 months, core PPI is running at an annualized rate of 8.2%.

The reason for the miss in PPI vs the estimate was the unexpected 4% drop in transportation/warehousing prices. Airline passenger services in particular saw a 17% drop but still up 4.4% y/o/y. Also, medical care costs were benign as were cell phone services and insurance. Trade pricing rose by .9% in the month.

Goods prices continued with its pretty aggressive increases, rising another .6% ex food and energy. Food was up 2% in the month alone while energy prices jumped by 2.8% in September. Auto’s/parts prices rose 3.4% and are up 91.2% y/o/y, yes almost a double. RV’s/Trailers/Campers prices rose 10.4% m/o/m and 18.5% y/o/y. Machinery price gains were also notable.

Specifically with freight, ‘truck transportation of freight’ prices rose .8% m/o/m and 15% y/o/y. Air transport prices jumped by 2.3% m/o/m and 5.2% y/o/y. Rail was higher by .4% m/o/m and 6.8% y/o/y.

Inflation in the pipeline looking at intermediate processed goods is up 23% ex food and energy in the last 6 months annualized. The early step before for unprocessed goods fell 3.5% m/o/m and was the only respite but are still up 17% annualized over the past 6 months.

Bottom line, thanks to a 17% drop in passenger service prices as stated, core PPI was below expectations with the headline about in line. Goods price gains remained pretty steady and keep in mind that if energy prices remain high, that will eventually filter into plastics, cement, petrochemicals, etc… that use oil and/or natural gas as a feedstock. I said earlier that the CRB raw industrials index is at a record high two weeks into October. I would thus take NO comfort in the print being below expectations.

The bond market agrees with me, for now, because the 5 and 10 yr inflation breakevens are at the highs of the day, each up another 2 bps.

CORE PPI y/o/y

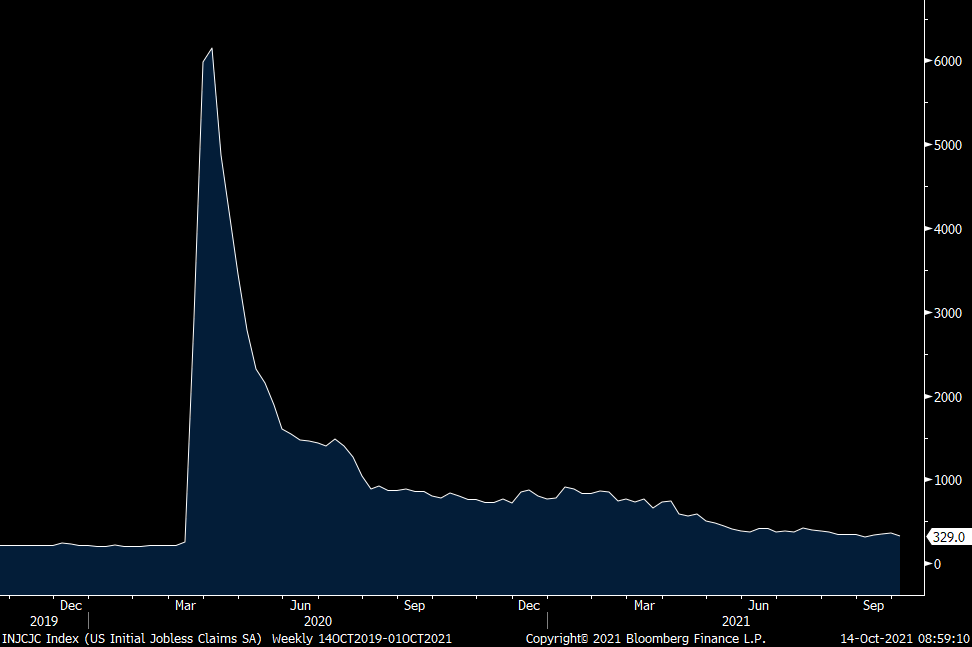

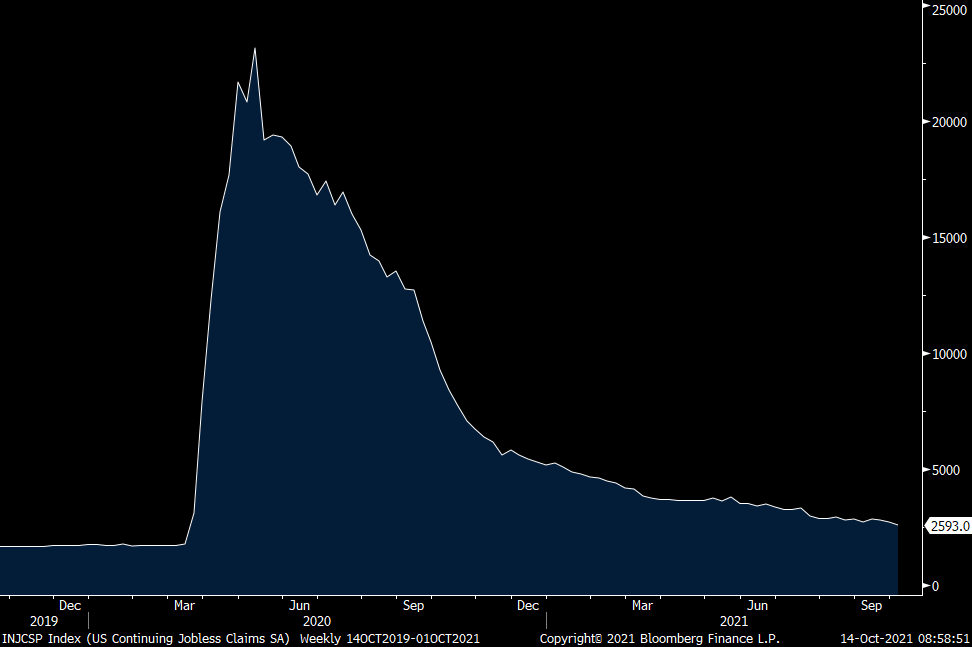

Initial jobless claims totaled 293k, below the estimate of 320k and down from 329k last week and finally a print with a 2 handle for the 1st time since pre Covid. The 4 week average fell to 334k from 345k. Also positive, continuing claims dropped by 134k w/o/w to 2.59mm and well below the estimate of 2.67mm and the lowest since pre Covid. They have now fallen by 259k since August as back to school and the end of extra unemployment benefits likely helped with that but to what extent is tough to measure. Either way, with more than 10mm job availabilities, it makes sense that we see continued declines in the pace of firing’s and those still receiving claims.

INITIAL CLAIMS

CONTINUING CLAIMS

Peter is the Chief Investment Officer at Bleakley Advisory Group and is a CNBC contributor. Each day The Boock Report provides summaries and commentary on the macro data and news that matter, with analysis of what it all means and how it fits together.

Peter is the Chief Investment Officer at Bleakley Advisory Group and is a CNBC contributor. Each day The Boock Report provides summaries and commentary on the macro data and news that matter, with analysis of what it all means and how it fits together.