In my decades in the markets I’ve learned to fade geopolitical worries and events as the impact is rarely lasting in terms of impacting economic activity. As I still believe Putin will not implement a full fledged invasion, I want to fade this too. That said, because commodity prices are as high as they are, any disruptions will really matter. Thanks to a friend (h/t RF), here are some important stats on the importance of Ukraine when it comes to industrial metals, energy and ag. 1)They are 1st in Europe with uranium proven reserves, 2)They are 2nd place in Europe and 10th in the world with their titanium ore reserves, 3)They have the 2nd most explored reserves of manganese ores in the world, 4)They have the 2nd most reserves of iron ore in the world, 5)They have the 2nd most reserves of mercury ore, 6)They have the 3rd largest reserves of shale gas in Europe and 13th place in the world, 7)They have the 7th most reserves of coal, 8)They have the most amount of arable land in Europe, 9)They are 1st in the world in the number of sunflower and sunflower oil exports, 10)They are the 2nd largest producer in the world of barley, 11)They are the 3rd largest producer of corn, 12)They are the 4th biggest maker of potatoes, 13)They are the 5th biggest producer of rye, 14)They are the 8th largest grower of wheat, 15)They are the 9th biggest producer of chicken eggs, 16)They are #16 in the world in cheese exports.

Any pullback in energy and ag on any easing of tensions, which is very likely, should be bought I believe as the supply/demand imbalances should persist.

After the Bureau of Labor Statistics last week told us that Rent of Primary Residence in the CPI figure was up 3.8% and the OER calculation was higher by 4.1% for January, CoreLogic said yesterday that US single family rental home prices, that include condos, were up 12% y/o/y in December. They said “Rent growth continued at a rapid pace for all price tiers in December.” They were higher by 36% in Miami in particular, leading the major cities. CoreLogic highlighted the problem here, that prices for home buying have become unaffordable for many young families and they in turn have to rent. “While slowing home price appreciation could help gradually balance demand for the rental market, rent prices will likely remain strong throughout the year.” This data compares with the Apartment List stat of rents up almost 20% y/o/y but that only calculates new rents as CoreLogic combines that plus renewals.

I’ll repeat again, inflation is NEVER transitory as seen in the CPI chart below and that is because the service component ALWAYS goes up. The swing factor then is for goods and we’ve of course seen what’s happened there over the past few years. Goods price gains though will moderate from here but the service side won’t.

US CPI Index, NEVER TRANSITORY

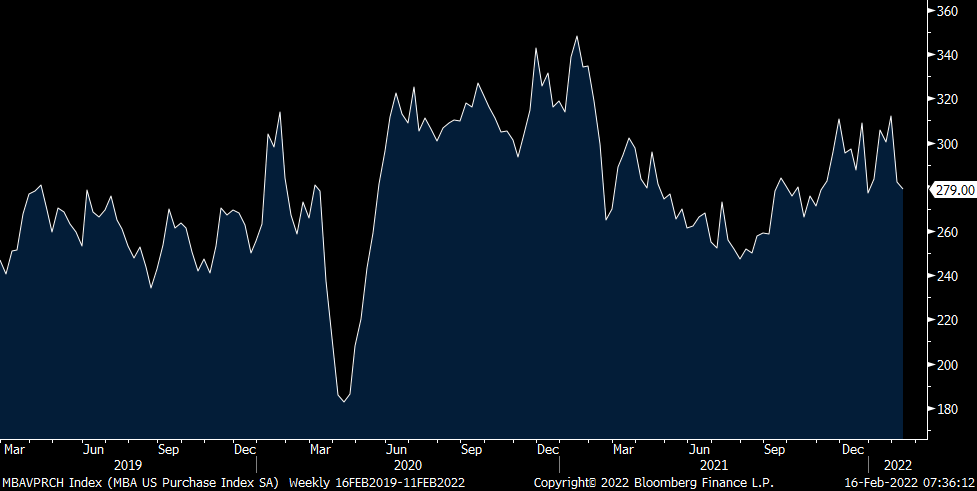

With respect to housing, the average 30 yr mortgage rate as of February 11th is above 4% at 4.05%. It was last there in November 2019 but you can imagine how many are now locked into a mortgage with a 3 handle after so many refi’s in 2020. Thus, they won’t be so quick to get out of that low priced mortgage in terms of providing home supply. Purchases fell 1.2% w/o/w after an almost 10% drop last week. They are down 7.3% y/o/y. Refi’s were lower by 9% w/o/w to the lowest since January 2020 and down 54% y/o/y.

REFI index

PURCHASE index

I forgot to mention the new January Cass Freight data that was released on Monday and the data was polluted by omicron. February thus should normalize. January shipments fell 2.9% y/o/y and were lower by 10.8% m/o/m. Blame omicron driven absenteeism and quarantines. Cass specifically said “This was not a demand driven decline, as inventories are still lean and consumer balance sheets strong.” While we see headlines of less containerships at the California ports, down to 78 as of February from a high of 109 in January, “per our friends at MX SoCal, backlogs have been growing at several other ports, particularly Houston, Charleston and Virginia.”

With respect to pricing, Cass Freight infers them by comparing shipments with total expenditures and here we see freight rates rose 35% y/o/y vs 33% in December. They were up by 3% m/o/m in January. They also said truck is taking share from rail “as the railroads continue to struggle.” This also adds to higher costs. With rail, “Chassis production has improved considerably for the past 6 months, but only enough to turn the direction of the chassis fleet from contraction to slight growth, and the chassis fleet remains far from what is needed to address rail network congestion.”

Bottom line here, and after listening to countless conference calls of company stocks we own and others, inflationary pressures might only improve slightly in the 1st half of 2022 and there is definite hope for more easing in the 2nd half but right now that is just hope. Companies are still planning to hike their own prices in a range of mid single digits to low double from what I’ve heard. Thus, to state AGAIN, the inflation rate of change will moderate from the likely peak in February or March but will still remain persistent and elevated this compared to the 1-2% we had become so accustomed to. In 2023, pressures should definitely ease much further but I can’t think about 2023 right now as there is way too much time and events to come between now and then.

China said its PPI rose 9.1% y/o/y in January, 4 tenths less than expected and vs 10.3% in December. The CRB raw industrials index did fall slightly in January. Also, there is a lot of commodity bullying going on in China from authorities there who pressure many to keep a lid on prices but I have no idea what influence, if any, that has on this data. Consumer price gains remain benign, up just .9% y/o/y vs the estimate of up 1% and vs 1.5% last month. A 3.8% drop in food prices kept a lid on things but even ex food and energy, prices were up just 1.2%. Obviously the very strict covid rules in China is likely capping inflation gains but who knows to what extent. The China 10 yr yield fell 1 bp to 2.78% so not much of a market mover was this data.

We also saw inflation data out of the UK. CPI was up 5.5% y/o/y in January headline and higher by 4.4% ex food and energy, both one tenth more than expected. The Retail Price Index, that inflation linkers use and are priced off, was higher by 7.8% y/o/y. On the wholesale side, producer input prices were up by .9% m/o/m and 13.6% y/o/y while output charges grew by 1.2% m/o/m and 9.9% y/o/y. The input side was just under expectations but the pass thru via output prices was much greater than expected with the m/o/m gain double the estimate.

As the data was about as expected and this is also raising the pressure on the BoE to hike 50 bps at their next meeting (something I don’t believe they’ve done since the 1990’s), inflation breakevens are falling with the 10 yr down by 2.7 bps to 4.06%. The 5 yr is down almost 4 bps to 4.17%. The BoE benchmark rate is currently at .50%. Gilt yields are lower. These numbers come with omicron driven slower price gains in travel/leisure will now certainly reverse itself higher.

With respect to the release of the FOMC minutes today, I’ll only send out a note if there is something new and important. We know the only question for the March meeting is whether they are hiking 25 bps or 50 bps and maybe we’ll get a timeline on QT. As there is still a month between now and then, why bother revealing clues right now in the minutes from a meeting 3 weeks ago.

Peter is the Chief Investment Officer at Bleakley Advisory Group and is a CNBC contributor. Each day The Boock Report provides summaries and commentary on the macro data and news that matter, with analysis of what it all means and how it fits together.

Peter is the Chief Investment Officer at Bleakley Advisory Group and is a CNBC contributor. Each day The Boock Report provides summaries and commentary on the macro data and news that matter, with analysis of what it all means and how it fits together.