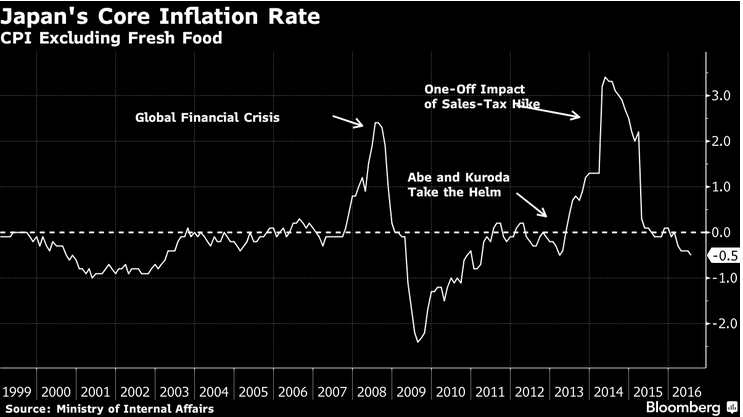

As hinted at over the past few months, the BoJ tweaked its monetary program to include “yield curve control.” They will do this by essentially setting the level of interest rates they want to target with the goal on the 10 yr yield in particular at around zero percent. They didn’t tell us however where they want the rest of the curve at. They chose not to go further down the rat hole of NIRP but of course left it open for more as they did with other options if current plans fail. They also took away a specific time frame on when they hope to achieve 2% inflation and replaced it with “at the earliest possible time.” As part of this, they will also have an ‘inflation overshooting commitment’ in which the Bank commits itself to expanding the monetary base until the y/o/y rate of increase in CPI exceeds the price stability target of 2% and stays above the target in a stable manner.” The etf stock purchases will continue.

Bottom line, the language on “yield curve control” was very vague. They want to steepen the yield curve but barely. With the short end at -.10% and their desire for a zero yield out 10 years, that is not very steep! The much longer end I guess will carry the burden but the BoJ will also be afraid to let those yields rise too much. Also, as they didn’t change the total amount of JGB’s they are buying, there is only so much control they can have over the longer part of the curve. With respect to the desire for higher inflation, I’ll say again, be careful what you wish for because interest rates will spike and economically speaking income growth is barely above zero. The market response was as follows: like a magnet the 10 yr JGB yield approached zero rising by almost 4 bps to -.027%. The 40 yr yield was up by 1 bp. The short end saw a rise in yields too by about 3 bps as the current level of NIRP was maintained. The Topix bank index spiked by 7% also on the hopes for a steeper yield curve (even though it doesn’t seem there will be much of one) and from not go deeper with NIRP. The yen is higher as there wasn’t any discussion I saw on it. The Nikkei rallied by 1.9% led by the banks as said. The BoJ has already lost control of the yen and its stock market and we’ll now see to what extent they can “control” longer term interest rates.

As for the Fed today, I believe Lael Brainard’s dovish speech a week ago Monday clinched no rate hike today as one has to go back to Wayne Angell’s tenure in the early 1990’s to have a rate hike with a Federal Reserve Governor dissenting. If Lael agrees to a rate hike today after what she said last Monday would be quite an about face and an embarrassing one. We’ll get an updated dot plot today but that has been rendered worthless information.

Bullishness continues to come out of market sentiment as measured by II. Bulls fell to 44.6 from 49 last week. That is a 3 month low after reaching above 55 only a month ago. Bears rose 1.7 pts to 24.3 to a 10 week high. Those expecting a Correction was up by 2.7 pts to 31.1. This new attitude certainly reflects the market turbulence seen on two days over the past few weeks.

Adding to the lumpy housing data, mortgage applications to buy a home fell by 6.8% w/o/w after rising by 8.6% last week. The y/o/y gain slowed to 3.3%. Refi applications fell by 7.6% to a 12 week low. This behavior was likely in response to the rise in mortgage rates to the highest level since early July. We saw a jump in builder sentiment on Monday, a weaker than expected starts number yesterday and a w/o/w decline in today’s high frequency data. Tomorrow we get a somewhat dated existing home sale number but we’ll be watching for the buying behavior of first time households.

Peter is the Chief Investment Officer at Bleakley Advisory Group and is a CNBC contributor. Each day The Boock Report provides summaries and commentary on the macro data and news that matter, with analysis of what it all means and how it fits together.

Peter is the Chief Investment Officer at Bleakley Advisory Group and is a CNBC contributor. Each day The Boock Report provides summaries and commentary on the macro data and news that matter, with analysis of what it all means and how it fits together.